As Integral Ad Science marks its fourth anniversary on the Nasdaq, speculation mounts over its future

Integral Ad Science, a publicly listed ad tech company with a market capitalization exceeding $1 billion, is the subject of a potential takeover by private equity, according to recent reports — but interest is wavering.

Today (June 30) marks the fourth anniversary of IAS’ initial public offering. Potential suitors sent out due diligence notifications to audit partners during the last quarter, albeit opinions are mixed as to the most likely outcome, according to Digiday sources.

KKR is out

Late last year, separate reports suggested that IAS was about to be taken private. Business Insider cited sources claiming that PE giant KKR was the firm, following an article from Bloomberg that reported it was exploring future options with Jefferies Financial Group.

In the six-plus months since those reports, KKR’s interest in buying IAS is understood to have expired, although additional PE firms have also expressed an interest in buying the ad verification outfit. These PE firms include Bain Capital, with PricewaterhouseCoopers understood to have facilitated such explorations earlier this year.

All sources consulted by Digiday requested anonymity to maintain their relationships with the concerned parties, but all three claimed such talks have taken place in recent months.

One source claimed KKR has revisited the conversation in recent weeks; another said talks had “fallen through.” Meanwhile, two separate sources told Digiday that rival PE firm Bain has also looked at a take-private deal, with memos circulated earlier in the year instructing partners to prepare for potential due diligence.

Alternate plans

However, such activity is understood to have cooled in recent weeks, although sources separately told Digiday that investment bank Jefferies is still trying to engineer a deal.

Meanwhile, a third, separate source told Digiday that bankers, separate from Jefferies, had discussed the potential divestiture of firms IAS acquired since its 2021 IPO, including Publica, an outfit it purchased for $220 million that year.

However, such discussions are understood to have stalled as a result of economic uncertainty stemming from the looming tariff policies from the U.S. administration led by President Donald Trump.

Representatives of IAS did not respond to Digiday’s request for comment at time of writing, nor did spokespeople for Jefferies and PwC.

Shailin Dhar, partner at Futureproof TMT, a research firm that advises potential acquirers in the space, told Digiday PE firms continue to explore the space even if the process often proves pricey and involves multiple parties.

“People say M&A in the media and ad tech space has been dead, but it’s not for a lack of trying. PE firms have been constantly putting new things on the board to explore what can work,” he explained. “In the past 18 months, only three of the 20 potential transactions that we have taken on actually made it into real technical diligence.”

The PE longview

Prior to listing on the public markets, IAS was owned by Vista Equity Partners, a firm with other interests in ad tech. It is still the largest shareholder in the ad verification company, owning approximately 40% of its stock.

Vista Equity Partners purchased IAS in 2018 using its Fund VI — a war chest it first raised from investors in 2016 — as observers noted that the PE firm would soon be expected to deliver ROI. The general wisdom is that PE funds have a general lifespan of 10 years, with the potential for year-long extensions if required due to market conditions — typically referred to as “10+1+1.”

Such funds typically hold onto portfolio companies for a five-to-six year window. Vista Equity Partners’ Fund VI will reach its 10-year initial term in 2026, at which point it will widely be expected to soon explore an exit.

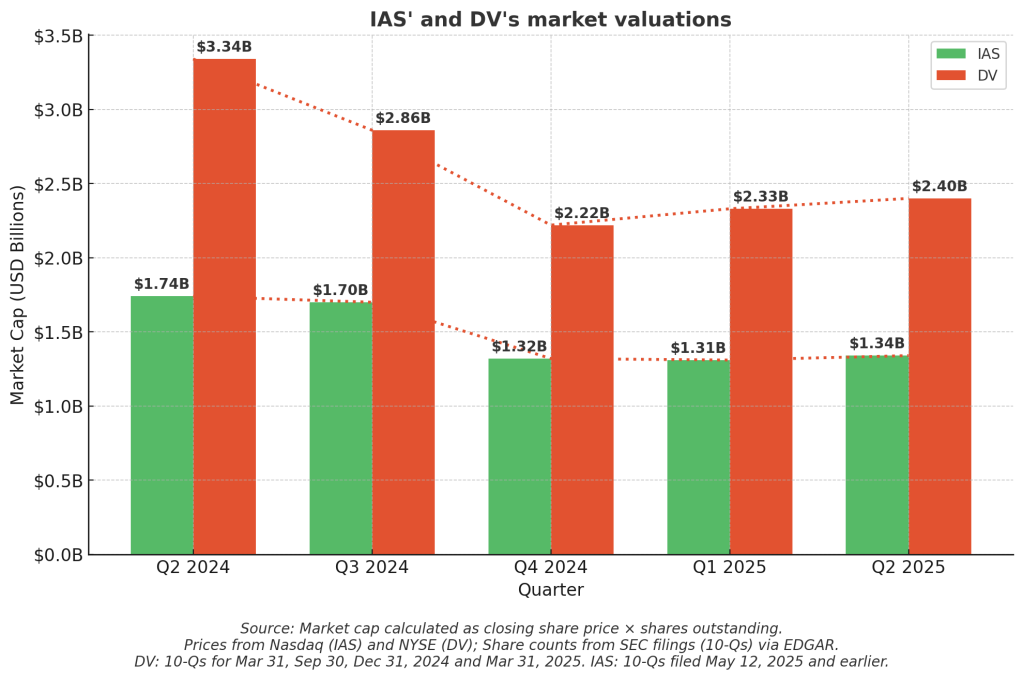

One source told Digiday there is a widespread perception that Vista Equity, which also purchased sell-side ad tech firm TripleLift using a separate fund, is keen to see a return on its IAS investment. Many point to the comparative success of its most direct market rival, DoubleVerify, as a reason for the PE firm’s purported eagerness to exit the investment. This is despite IAS regularly delivering double-digit revenue increases during its time on the public markets.

At the time of writing, in late June 2025, IAS’ market capitalization was $1.07 billion, compared to DoubleVerify’s $2.36 billion, according to pricing information sourced from their public listings on the Nasdaq and NYSE, respectively.

However, the ad verification and measurement space as a whole is under pressure, with class action lawsuits against the likes of DoubleVerify adding fuel to the growing scrutiny from lawmakers.

Many advertisers are scrutinizing verification vendors’ claims about the robustness of their technological capabilities, plus there are growing challenges from market interlopers, such as Mobian and Scope3. Additionally, there is the longstanding criticism of the role such companies play in depriving traditional media outlets of ad revenue.

However, IAS management is making moves suggesting it is business as usual. Earlier this month, it announced the updated the terms of its loan deal with a group of banks. This included a loan extension, meaning its existing credit line was extended by five more years — it now runs until June 2030 – which gives the company more time to access and repay borrowed funds.

The terms also include an enlarged borrowing limit, meaning IAS can now borrow up to $550 million, up from its earlier $300 million, with the banks’ agreement. According to IAS, this shows it’s planning ahead for future needs while still sitting on a healthy amount of cash — it had $59 million in cash as of the end of March 2025.

More in Media Buying

Omnicom CEO: ‘The marketplace hasn’t seen what the cost of this AI is’

Omnicom CEO John Wren just said the quiet part out loud: nobody’s actually priced AI yet.

Media Buying Briefing: Why Omnicom merged Mediahub and Hearts & Science

Merging Hearts & Science and Mediahub into one agency that will operate under a new name and brand may not be the last move the holding company makes in simplifying its go-to-market offering.

Google quietly gives ground on PMax controls

The search giant’s black-box ad product has confounded media buyers for years. Now, it’s passing them the reins – sort of.