Prices rise for the Digiday Programmatic Marketing Summit after Mar. 24

Media and creative agencies face a range of threats in 2026, from generative AI to media fragmentation and the continued dominance of Meta and Google’s platforms.

In response, few businesses in this sector have stood still. They’ve chosen to merge, acquire — or in the case of Dentsu, cast loose — to keep moving forward. The likely destination? A leaner sector that employs fewer people and trades on its tech bonafides and principal-media trading capabilities over its creative chops.

In the graphs below, we’ve brought together five different ways of seeing the agency sector as things stand now.

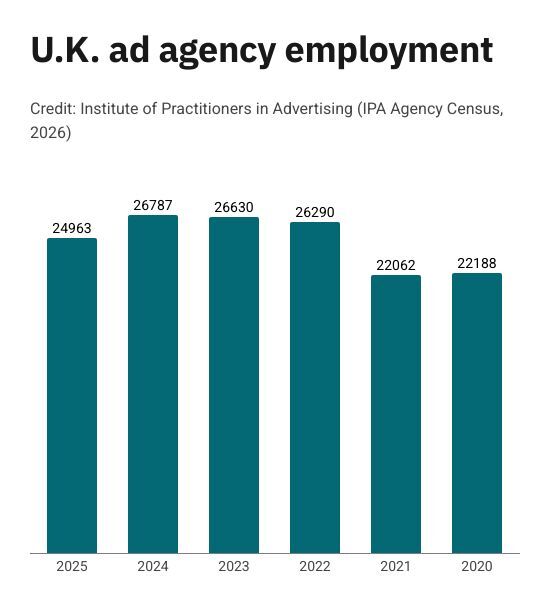

Industry headcounts are falling

Credit: IPA Census 2025

It’s not difficult to find examples of agencies cutting headcount. Omnicom, for example, shed thousands of staff positions in the last year; as of its latest earnings call, the company’s leadership plan to pursue hundreds of millions of dollars more in “synergies”.

Employment figures published by Britain’s Institute of Practitioners in Advertising (IPA) this month show a long-term trend playing out. Agencies staffed up during the pandemic years, but are now tightening their belts, leaving fewer jobs available.

At least some of that is in response to AI; 24% of British agencies expect to cut staff this year as a result of the technology, according to the IPA’s annual Census study.

No more ‘Big Six’

Consultancy MediaSense’s “Agency Family Tree” shows a sector as tangled up as a medieval European dynasty. But while executives’ yearning to consolidate their portfolios might render it out of date within a few short months, it’s a snapshot of the industry as things currently stand (you might be best zooming in, though).

The popular six-sided understanding of the holding company landscape has been demolished in the last 12 months. Omnicom has swallowed Interpublic Group, and now only Publicis Groupe and WPP register comparable revenue figures. Meanwhile, Stagwell has grown since its own blockbuster acquisition of agency network MDC in 2021; as the Family Tree shows, it now boasts an agency roster, and annual revenues, to rival that of French group Havas.

The result? A two tiered industry dominated by the “operating companies” trailed by challenger holding companies and filled out by independents, mid-sized networks (think MSQ) and consultancy players.

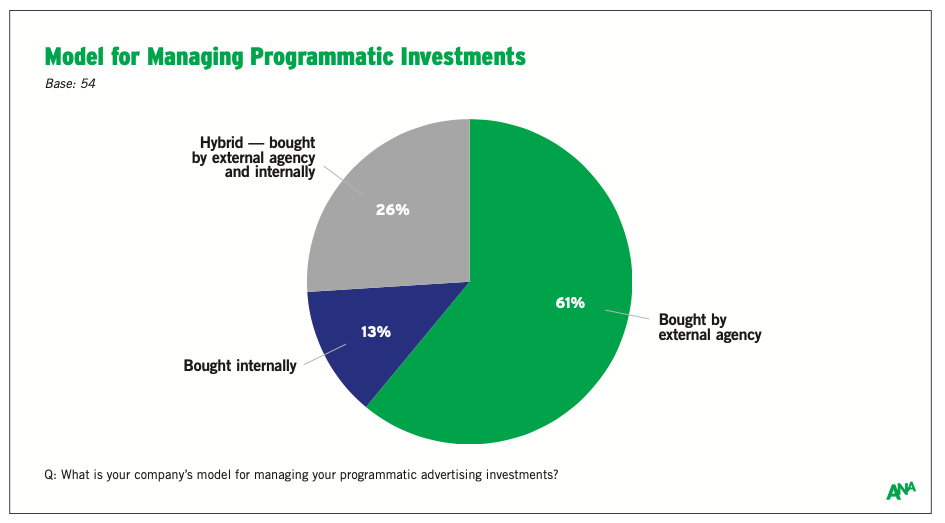

In-housing continues apace

Credit: Association of National Advertisers

In-housing has been a concern for agency execs for over a decade. Agencies have always needed to work to prove their worth to clients, but over the last decade some of the industry’s biggest advertisers (exactly the kind of companies that underwrite big agencies) have begun to go it alone.

While some companies stopped at bringing some creative marketing spending inside, others have gone as far as building out their own media units — some of which employ their own programmatic traders.

While few companies have in-housed absolutely every marketing function, the end result is that there’s less work to go around. It’s a trend most observers expect to become more acute as generative AI enables small teams to do more with their time.

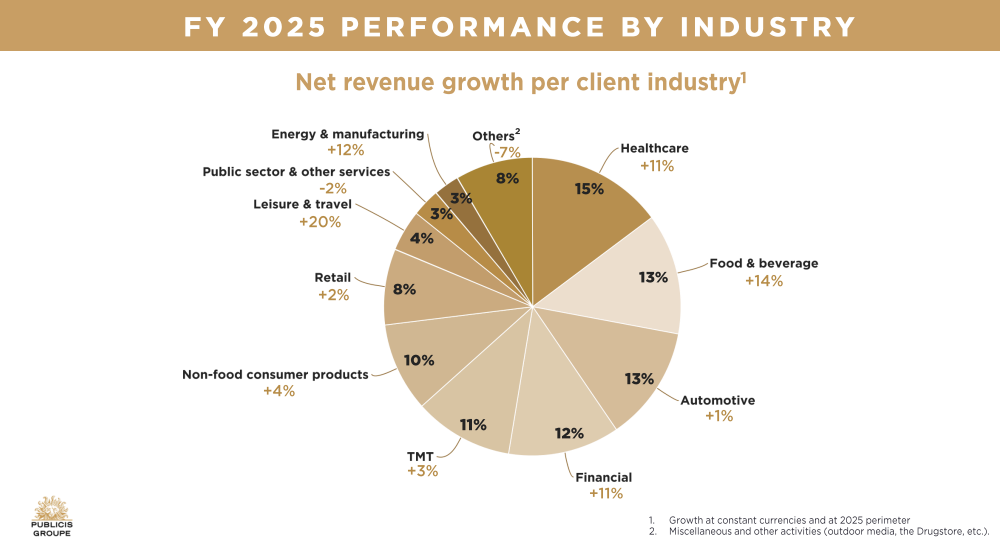

Pharma ads pay the bills

Credit: Publicis Groupe, 2025 full year earnings presentation

Automotive brands still have an allure for ad execs. But the days when a carmaker could make or break an ad agency are long gone.

In 2025, for example, most of Publicis Groupe’s revenues came from pharmaceutical and healthcare clients such as GlaxoSmithKline and Pfizer. The category’s big players increased ad spend during the pandemic and have doubled down as they attempt to harness consumer demand for GLP-1 drugs.

Meanwhile, automotive spending grew just 1% last year, versus 11% from healthcare clients, 14% from food and beverage and 20% among leisure and travel clients. Public sector and government spending has been gradually declining in most countries, following the glut of investment required from public health bodies in the Covid-19 years.

They’re still prepared to acquire

Credit: Havas, 2025 full year earnings presentation

Holding companies acquired to grow in years past, and many of the decisions being taken by today’s execs are in direct response to the problems that strategy brought.

But the industry’s biggest players are still prepared to grow through acquisition. Havas, for example, only recently a public company, has already brought two companies into the fold this year and acquired 11 in 2025. And Publicis hasn’t been far behind, having bought several agencies and tech companies over the last three years.

More in Marketing

Retailers turn to digital rebates as alcohol sales slump

Grocers and C-stores are turning to digital alcohol rebates to try to boost alcohol sales and digital engagement.

Advertisers aren’t happy about picking up Meta’s European tax tab

As things stand, Meta hasn’t provided any communication to ad execs about these additional fees, beyond the email shared with Digiday.

Ad Tech Briefing: The industry is rethinking its foundations as a new world order is established

The days of ‘fake it ’til you make it’ are coming to an end.