The race to the single platform has begun: Who will finish first, and who won’t finish

By Pat McCarthy, SVP, Corporate Marketing, AppNexus. The opinions here are his own.

Earlier this year, Terrence Kawaja, well-known investment banker and ad tech divinator, rattled many nerves when he predicted an imminent wave of consolidations and failures in the ad tech sector. Of the roughly 2,000 companies involved in advertising technology, he estimated that no more than 150 will live to see a successful liquidity event. The others will either be swallowed whole by as many as 15 mega-platforms or fail altogether.

Speaking as an industry veteran, I largely agree with Kawaja’s assessment. What I increasingly hear from customers, peers, journalists and analysts is that the chaotic ad tech landscape is poised to undergo a period of creative disruption and consolidation. Out of this process, a small number of single-platform companies will emerge, able to provide “end-to-end” technology for both buyers and sellers of digital inventory.

In effect, these single-platform technology partners will forge highly liquid and efficient marketplaces that power the exchange of digital inventory across multiple formats (like video and display) and devices (desktop, mobile, tablet); they will be able to facilitate both real-time bidding and automated guaranteed buying and selling. Publishers will look to single-platform providers for holistic yield management and analytics, while advertisers will demand that they give them control of their data and decision-making.

This isn’t to say that there won’t be a place in the ecosystem for point-solution providers. Building single-platform technology is expensive and complicated. Not every ad tech company can or should endeavor to build a full stack. For both single-platform providers and point-solution survivors, the market – which is to say, the combined judgment of publishers, agencies and advertisers, analysts and investors – will ask tough questions and set high bars.

The market will ask single-platform companies whether they built their technology stacks organically, or whether they stitched them together from various acquisitions along the way. Most likely, no company will have created its single-platform solution entirely from scratch, or entirely by acquisition. But the “hackiest” platforms –those whose component parts never quite fit together correctly – will suffer for lack of speed, complicated integrations, inadequate reporting, and insufficient buy-side liquidity.

Likewise, the market will demand proof of scale and reach, and – most importantly – the commoditization of services and lower prices. Simply put, once they have completed their technology stacks, single-platform providers won’t be able to charge the same take rates as niche point-solution partners. The entire rationale for migrating one’s business to a single platform is to achieve efficiency and economies of scale. The days of double-digit take rates as the industry standard are soon to be a thing of the past. Those companies—single-platform or otherwise – that haven’t built this reality into their business models might find themselves in a world of trouble.

Finally, the market will demand more visibility into pricing, performance and inventory quality. The move to single-platform solutions will only benefit content producers and advertisers if it results in a more transparent ecosystem.

Surviving point-solution providers will field tough questions. For one, can they demonstrate that their specialized technology offerings enhance– rather than complicate or duplicate – the single-platform systems? Are they allowing for buying and selling across different formats and marketplaces, or offering specialized forecasting, data management and analytics that the single-platform players don’t offer? Can they plug into the larger platforms without creating undue layers of script and code, avoiding the familiar problems of latency and load time? Finally, can they survive in a world of price compression and commoditization?

In its short lifespan, ad tech has always been a hyper-competitive industry. The stakes have never been higher. The programmatic market is expected to grow at 20 percent annually between 2015 and 2018 – outpacing every other category of digital and non-digital advertising, according to Magna Global. The race to the single platform has begun. How it shakes out is the question we’ll all be asking.

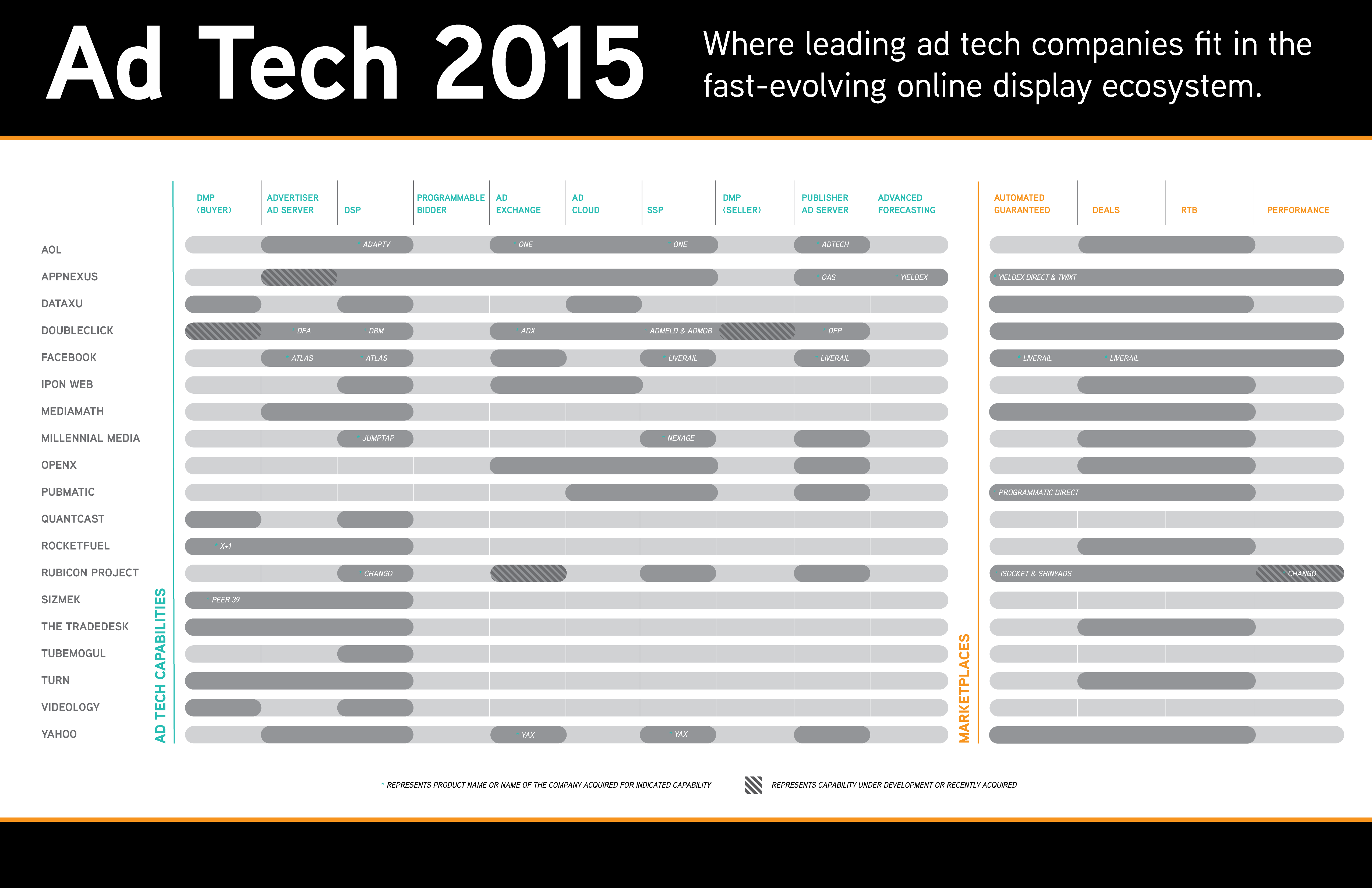

(Note on graphic: This visualization attempts to illustrate the race to the single-platform solution. My colleagues and I drew from our collective industry knowledge and anticipate that we may be missing certain details that are proprietary to various industry actors. We invite feedback and commentary, as the industry is ever-changing and dynamic, and few people have full visibility into the whole ecosystem.)

More from Digiday

Michaels claims Google-powered AI assistant doubles conversion rate of traditional search

Michaels shared early results of its new Google Gemini-powered AI assistant.

Mythbusters: AI visibility’s biggest misconceptions

AI visibility is evolving quickly, but many of the industry’s biggest assumptions don’t hold up. Experts debunk the biggest myths.

Kai Cenat’s Streamer U was a ‘masterclass’ for brands looking to tap content creators

The creator bootcamp brought in big brand partnerships and big engagement metrics, which could bring more brands to the streaming sponsorship table.